Europe Virtual Reality Market Size

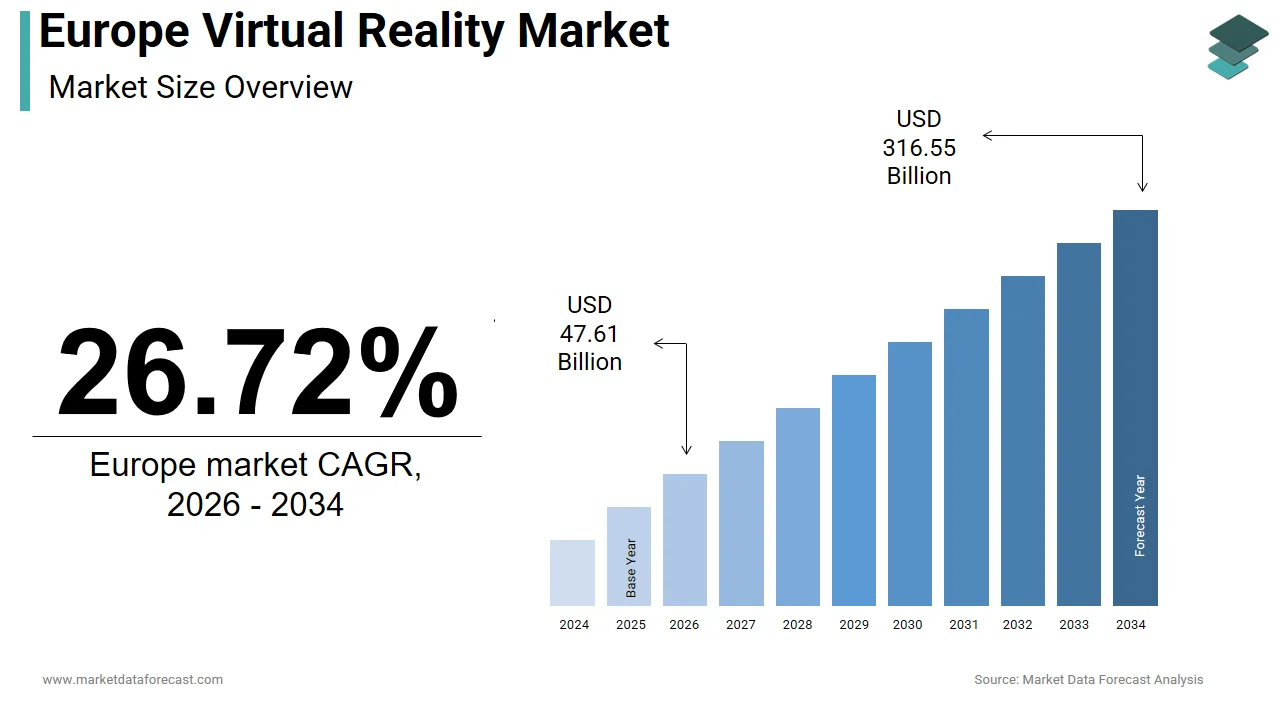

The Europe virtual reality market was valued at USD 29.65 billion in 2024, is estimated to reach USD 37.57 billion in 2025, and is projected to reach USD 249.82 billion by 2033, growing at a CAGR of 26.72% from 2025 to 2033.

Virtual reality refers to the immersive technologies that simulate three-dimensional environments through head-mounted displays, motion tracking, and spatial audio systems. These technologies enable users to interact with digital spaces in real time across entertainment, enterprise, healthcare, and public sector applications. Europe’s VR ecosystem is distinguished by strong regulatory frameworks for data privacy, robust academic research in human-computer interaction, and early adoption in industrial training and medical simulation. As per research, virtual reality (VR) is increasingly being researched and used for surgical planning and patient rehabilitation in some European hospitals. National initiatives further accelerate integration. Europe’s VR adoption is primarily led by enterprises and institutions, rather than consumers, like in other markets. This is influenced by policy support, a focus on digital sovereignty, and a human-centric approach to immersive technology design.

MARKET DRIVERS

Integration of Virtual Reality in Industrial Workforce Training and Digital Twins

European industries are increasingly adopting VR to address skilled labor shortages and enhance operational safety through immersive simulation, which boosts the growth rate of the Europe virtual reality market. According to studies, a portion of manufacturing and energy companies in the EU used VR for technician training in 2023, which reduces onboarding time by an average of 35 percent. Siemens Energy utilizes digital twin technology and VR environments for technician training, an innovation that helps reduce the need for physical prototypes and is referenced in the company’s sustainability reports as part of its digitalization efforts. The European Union Aviation Safety Agency (EASA) approves the use of Virtual Reality in aviation training, including for flight simulators and procedural practice. This convergence of regulatory compliance, cost efficiency, and safety imperatives is transforming VR from a novelty into a core component of Europe’s industrial resilience strategy.

Adoption of Virtual Reality in Clinical Therapy and Medical Education

It is gaining clinical legitimacy as a non-pharmacological intervention for mental health and a pedagogical tool in medical training is fuelling the expansion of the Europe virtual reality market. Virtual reality technologies are gaining wider adoption across hospitals in Europe for mental health treatments such as anxiety disorders and trauma rehabilitation, according to studies. Regulatory bodies across Europe are increasingly recognizing the role of VR applications in medical research and clinical evaluations, accelerating their integration into standardized healthcare practice, according to studies. These institutional endorsements validate VR’s therapeutic efficacy and embed it within Europe’s public health infrastructure.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Under the General Data Protection Regulation

The European Union’s General Data Protection Regulation imposes significant constraints on virtual reality applications that collect biometric and behavioral data. This limits data-driven personalization and cloud-based analytics, which in turn restrains the growth of the European virtual reality market. According to research, biometric data, including eye tracking, head movement patterns, and physiological responses captured by VR headsets, are classified as special category data requiring explicit user consent and purpose limitation. Also, the enforcement actions deter innovation in adaptive learning and emotion recognition features that rely on continuous behavioral feedback. Moreover, multinational developers must implement region-specific data architectures. The consequence of these user rights requirements is a more difficult development process and a splintered European VR landscape, distinct from global platforms.

Limited Consumer Adoption Due to High Hardware Costs and Ergonomic Barriers

Hardware limitations and pricing barriers also impede the expansion of the Europe virtual reality market. According to sources, only a share of households in the EU owned a VR headset, with ownership concentrated in Nordic and Benelux countries. Ergonomic issues further discourage prolonged use. As per research, a portion of users experienced eye strain or neck discomfort after several minutes of continuous VR use due to headset weight and display latency. Content scarcity compounds the problem. Retailers have reduced in-store VR demo stations, citing low conversion rates. Consumer VR will remain a niche segment in the European digital entertainment landscape because of the lack of breakthroughs in lightweight optics, wireless rendering, and localized content production.

MARKET OPPORTUNITIES

Expansion of Virtual Reality in Public Sector Education and Cultural Heritage

European governments are leveraging VR to democratize access to education and preserve intangible cultural heritage through immersive storytelling, which provides fresh opportunities for the growth of the Europe virtual reality market. According to studies, several education ministries across Europe are increasingly embedding virtual reality tools into school curricula to enhance learning in subjects like science, history, and vocational training. As per sources, Italy has developed immersive heritage-based experiences that enable students to explore cultural landmarks through VR platforms integrated into classroom learning. As per sources, funding programs in the European Union continue to support collaborative VR-based initiatives focused on education and cultural preservation across member states. These initiatives position VR not as entertainment but as a public good, enhancing educational equity and cultural continuity across diverse linguistic and geographic communities.

Growth of Virtual Reality in Remote Collaboration and Hybrid Work Infrastructure

The normalization of hybrid work models has caused enterprise investment in VR-based collaboration platforms that replicate physical presence and spatial interaction, thereby opening major prospects for the expansion of the Europe virtual reality market. The European Central Bank uses VR for cross-national policy simulations where economists manipulate 3D data visualizations in shared virtual rooms, improving consensus-building during rate decisions. Architectural firms like Foster and Partners in London conduct client reviews in VR, allowing real-time material and lighting adjustments without physical mockups. Improved bandwidth, enabled by 5G and fiber, is driving the evolution of spatial computing from a mere novelty into crucial infrastructure for Europe’s distributed knowledge economy.

MARKET CHALLENGES

Fragmented Technical Standards and Interoperability Gaps Across Platforms

The absence of unified technical standards for virtual reality content and hardware in the region impedes cross-platform compatibility and scalable deployment, which ultimately holds back the expansion of the Europe virtual reality market. Multiple proprietary VR development platforms currently coexist across the European market, creating challenges for standardization and cross-platform compatibility, according to studies. This fragmentation forces developers to rebuild applications for each headset. Game developers in the region continue to allocate a significant portion of their resources to adapting products for different systems rather than advancing new creative features, as per sources. Public institutions face similar hurdles. The lack of standardized spatial audio and haptic feedback protocols further degrades user experience consistency. A fragmented European VR ecosystem, rather than a cohesive digital environment, is the inevitable result of a lack of a unified architecture.

Insufficient High Bandwidth Connectivity in Rural and Peripheral Regions

Uneven broadband infrastructure, particularly in Southern and Eastern member states, hampers the rise of Europe’s virtual reality market. This affects the performance of cloud-rendered and multiplayer virtual reality applications in Europe. According to research, in 2023, data from Eurostat indicated that the gap in internet access between urban and rural areas was far smaller. The digital divide excludes peripheral regions from VR-enabled services. Moreover, telemedicine has expanded in Greece, and network speed disparities exist. The spatial computing revolution will bypass rural Europe unless the Digital Europe Programme allocates specific funds for fiber backhaul and edge computing.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Device, Technology, Component, Application, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Alphabet Inc., Barco NV, CyberGlove Systems, Inc., Meta Platforms Inc., HTC Corporation, Microsoft Corporation, Samsung Electronics Co., Ltd., Sensics, Inc., Sixense Enterprises, Inc. (Penumbra, Inc.), and Ultraleap Ltd. |

SEGMENTAL ANALYSIS

By Device Insights

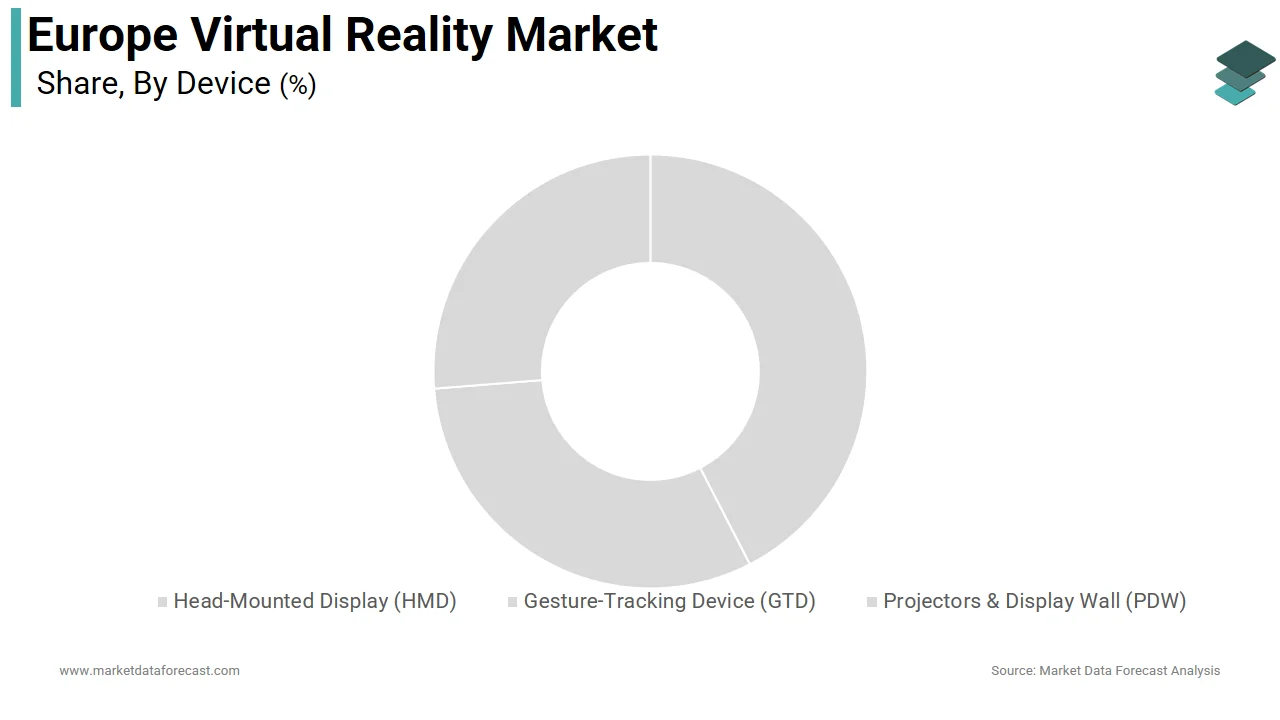

The head-mounted displays (HMD) segment held the majority share of the Europe virtual reality device market in 2024. Its ability to deliver true stereoscopic vision, head tracking, and audio spatialization, essential for both professional simulation and consumer engagement, has largely contributed to the prominence of the Head Mounted Displays (HMD) segment. Enterprise adoption is particularly robust. In a clinical setting, the UK’s National Health Service deploys HMDs in VR therapy clinics where patients confront anxiety triggers in controlled environments. Academic institutions reinforce this trend. Consumer uptake, though modest, is concentrated in HMDs with gaming and fitness applications driving sales in Germany and the Netherlands. The ergonomic and optical advancements in standalone models have rendered desktop tethered systems largely obsolete for new deployments across the continent.

The glasses type isplays (GTD) segment is on the rise and is expected to be the fastest growing segment in the global market by witnessing a CAGR of 34.1% share in 2024. The rapid expansion of the Glasses Type Displays (GTD) segment is fueled by the emergence of lightweight optical waveguide displays that blend digital overlays with real-world vision, enabling all-day enterprise use. Academic research is accelerating adoption. The European Defence Agency is also evaluating GTD for soldier situational awareness under its Future Combat Systems program. A more accessible form factor and longer battery life are enabling GTD to evolve from a niche tool into a mainstream spatial interface for the industrial and defense sectors.

By Technology Insights

The semi-immersive VR segment dominated the Europe virtual reality market by capturing a substantial share in 2024. The dominance of the semi and Fully Immersive VR segment is mainly driven by their capacity to deliver deep engagement through head-mounted displays, motion tracking, and spatial audio, important for enterprise and clinical applications. Some automotive manufacturers use semi-immersive CAVE environments for collaborative vehicle design reviews, reducing physical prototyping cycles, as per studies. The EU’s Horizon Europe program has allocated funds to advance haptic feedback and eye tracking in immersive systems, further cementing their technical and functional superiority over non-immersive alternatives.

The fully immersive VR segment is likely to experience the fastest CAGR of 29.4% share in 2024. The rapid growth of the fully immersive VR segment is fuelled by breakthroughs in standalone headset performance and enterprise demand for presence-rich collaboration. As per sources, several financial institutions in Europe are adopting immersive VR technologies to enhance analytical efficiency and collaborative decision-making. According to studies, universities across Northern Europe are integrating virtual labs into science education, helping improve student engagement and concept retention. Medical institutions are also advancing. The rollout of 5G standalone networks across urban Europe enables low-latency cloud rendering,` eliminating tethering constraints. These converging enablers position fully immersive VR as the cornerstone of Europe’s spatial computing future.

By Component Insights

The hardware segment accounted for a 62.8% share of the Europe virtual reality market in 2024. The capital-intensive nature of VR deployment, where headsets, tracking sensors, and computing infrastructure constitute the primary expenditure, has boosted the expansion of the hardware segment. Enterprise buyers typically allocate a portion of their VR budget to hardware, as per research, particularly in industrial and medical settings requiring high-fidelity displays and motion capture. Public institutions follow similar patterns. The shift to standalone headsets has further concentrated spending on integrated hardware. Apart from these, hardware longevity drives replacement cycles.

The software segment is expected to exhibit a noteworthy CAGR of 31.7% during the forecast period, owing to the rising demand for specialized applications in training simulation therapy and spatial collaboration that require continuous updates and customization. The European Aviation Safety Agency is increasingly approving Virtual Reality (VR) solutions for aviation training, including for cabin crews. In healthcare, Oxford VR developed automated cognitive therapy delivered via virtual reality, which was tested in several clinical trials within the UK’s National Health Service. Industrial software is equally dynamic. Bosch uses Virtual Reality (VR), Augmented Reality, and other digital solutions for maintenance and manufacturing, and offers cloud-connected platforms like the Nexeed Industrial Application System to manage tasks. In Europe’s maturing virtual reality (VR) ecosystem, software has emerged as the primary source of competitive advantage and profitability as hardware components become commoditized.

COUNTRY-LEVEL ANALYSIS

Germany Virtual Reality Market Analysis

Germany outperformed other regions in the European virtual reality market and occupied 24.7% of the regional market in 2024. The prominence of Germany is mainly propelled by industrial integration, where VR is embedded in manufacturing energy and automotive workflows. As per sources, major industrial companies in Europe are increasingly implementing large-scale VR training programs to enhance workforce efficiency and accelerate skill development. According to studies, research institutions in Germany are at the forefront of innovations in immersive learning, focusing on advanced sensory technologies such as haptics and eye tracking. As per sources, public education systems in Germany are also rapidly adopting VR tools for vocational training, particularly in technical and safety-oriented learning environments. The German Aerospace Center uses VR for astronaut training in collaboration with ESA. Germany is the powerhouse of European VR innovation, leveraging strong policy support, significant R&D, and extensive industrial digitization to produce practical applications and demonstrate engineering excellence.

United Kingdom Virtual Reality Market Analysis

The United Kingdom is the next major region of the Europe virtual reality market by accounting for 19.1% share in 2024. The growth of the United Kingdom is led by its clinical and creative prominence. The National Health Service runs VR therapy clinics nationwide using Oxford VR’s platform to treat anxiety and psychosis, with clinical trials showing symptom reduction after sessions. The UK is also Europe’s largest producer of VR content. Academic institutions like University College London pioneer neuroadaptive VR that adjusts scenarios based on real-time EEG feedback. Despite Brexit, the UK maintains strong ties to EU research programs, ensuring continued influence in both therapeutic and entertainment VR domains.

France Virtual Reality Market Analysis

France is an attractive region in the European virtual reality market due to its national strategy for digital education and defense simulation. Thales uses VR extensively for fighter pilot training with its TopSim platform, replicating Rafale cockpit operations for the French Air Force. Cultural institutions are equally active. The French National Centre for Scientific Research operates one of Europe’s most advanced VR labs for cognitive science, studying spatial memory and navigation. France is a prime example of a holistic national approach to immersive technology, with its government coordinating investment and ensuring cross-sectoral deployment.

Sweden Virtual Reality Market Analysis

Sweden is moving ahead steadfastly in the Europe virtual reality owing to its human-centered design and public health integration. The country mandates VR-based safety training in all construction and mining sectors following a 2021 occupational safety directive that reduced workplace incidents within a few years. Swedish game studios lead European VR content creation with titles available on all major platforms. Academic collaboration is strong. Sweden’s emphasis on ethical design, privacy by default, and public welfare ensures its VR ecosystem prioritizes user well-being alongside technological advancement.

Netherlands Virtual Reality Market Analysis

The Netherlands is anticipated to grow in the Europe virtual reality market over the forecast period due to its logistics and agritech applications. Port of Rotterdam uses VR to train crane operators in simulated storm conditions, reducing accident risk. Agricultural universities deploy VR to teach precision farming techniques. Philips Healthcare integrates VR into the radiology workflow, allowing doctors to explore 3D organ reconstructions before surgery. The Netherlands Organisation for Applied Scientific Research runs a national VR testbed for SMEs, providing subsidized access to enterprise-grade systems. The Netherlands has demonstrated scalable VR integration in various industries by focusing on practical, sector-specific deployment and fostering strong public-private partnerships.

COMPETITIVE LANDSCAPE

Competition in the Europe virtual reality market is characterized by a dual structure featuring global technology giants and specialized European innovators. Large players like Meta and Microsoft dominate through hardware scale and ecosystem integration, while Nordic and German startups such as Varjo and Immerse excel in high-fidelity professional applications. The market is highly application-driven with minimal consumer competition compared to North America or Asia. Public sector procurement plays a decisive role as governments mandate VR in education, healthcare, and defense, creating stable demand channels. Regulatory compliance, particularly around data privacy and medical device certification, acts as a significant barrier to entry, favoring established players with compliance infrastructure. At the same time, open source initiatives and EU-funded research projects foster collaboration among smaller firms. The absence of dominant local hardware manufacturers creates dependency on imports, yet European software developers lead in therapeutic and industrial content. This ecosystem rewards specialization, regulatory agility, and public-private alignment over pure technological scale.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe virtual reality market include

- Alphabet Inc.

- Barco NV

- CyberGlove Systems, Inc.

- Meta Platforms Inc.

- HTC Corporation

- Microsoft Corporation

- Samsung Electronics Co., Ltd.

- Sensics, Inc.

- Sixense Enterprises, Inc. (Penumbra, Inc.)

- Ultraleap Ltd.

Top Players in the Market

- Meta Platforms Inc. is a pivotal force in the Europe virtual reality market through its Quest series of standalone headsets and enterprise software ecosystem. The company supplies hardware and collaboration platforms to major European organizations, including Siemens, Deutsche Telekom, and the UK National Health Service. Meta has deepened its European footprint by establishing a dedicated enterprise support center in Dublin and launching localized VR training content in German, French, and Dutch. The company also partners with European universities to advance research in social VR and accessibility. These initiatives reinforce Meta’s role as an enabler of scalable immersive solutions across industrial healthcare and educational sectors throughout Europe and globally.

- Microsoft Corporation exerts significant influence in the European virtual reality landscape through its HoloLens mixed reality devices and Mesh collaboration platform. The company serves critical infrastructure sectors, including energy, healthcare, and defense, with solutions deployed at Airbus, BMW, and the German Aerospace Center. Microsoft has strengthened its European position by integrating Azure cloud services with spatial computing to ensure GDPR compliant data handling. The company also collaborates with EU-funded research consortia on digital twin and remote assistance applications. Through its enterprise-focused strategy and deep integration with existing Microsoft productivity ecosystems, Microsoft anchors mission-critical VR deployments across the continent and beyond.

- Varjo Technologies is a Finnish innovator renowned for its high-resolution human eye resolution virtual and mixed reality headsets used in professional simulation and training. The company supplies its XR 4 and Aero devices to European aerospace, automotive, and defense organizations, including Airbus, Volvo, and the Finnish Defence Forces. Varjo differentiates itself through photorealistic visual fidelity and precise eye tracking, enabling applications such as pilot training and surgical rehearsal. Varjo’s commitment to premium performance and regulatory compliance positions it as a leader in high-end professional VR both in Europe and global markets.

Top Strategies Used by the Key Market Participants

Key players in the Europe virtual reality market are prioritizing enterprise-grade security and compliance with the General Data Protection Regulation to build trust among institutional buyers. They are developing industry-specific applications in manufacturing, healthcare, and education rather than focusing solely on consumer entertainment. Strategic partnerships with national governments and public institutions are being forged to embed VR into vocational training and public health programs. Companies are investing in cloud-based streaming and 5G optimization to overcome hardware limitations and enable device-agnostic access. Localization of content in major European languages and alignment with national digital education strategies are enhancing adoption. Simultaneously, there is a strong emphasis on interoperability through open standards like OpenXR to reduce vendor lock-in. These strategies collectively address Europe’s unique regulatory, cultural, and operational requirements while enabling scalable and sustainable growth.

MARKET SEGMENTATION

This research report on the Europe virtual reality market has been segmented and sub-segmented into the following categories.

By Device

- Head-Mounted Display (HMD)

- Gesture-Tracking Device (GTD)

- Projectors & Display Wall (PDW)

By Technology

- Semi & Fully Immersive

- Non-immersive

By Component

By Application

- Aerospace & Defense

- Consumer

- Commercial

- Enterprise

- Healthcare

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

link